Repair or Replacement Coverage: A Practical Side-by-Side Guide

An analytical comparison of repair vs replacement coverage, with a clear framework to choose the right protection for homeowners and renters. Learn how to evaluate scope, costs, and claim processes to maximize value.

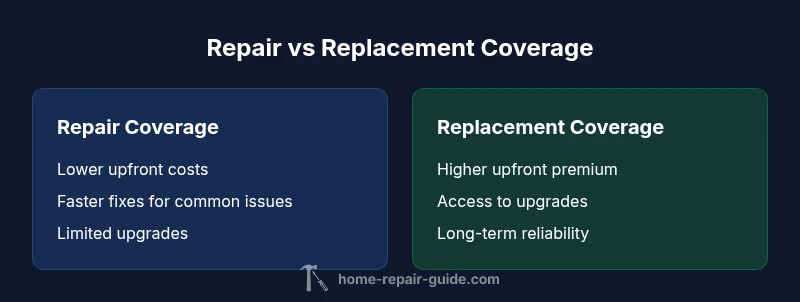

When choosing repair or replacement coverage, the quick takeaway is: repair-focused coverage minimizes upfront risk and speeds fixes for common failures, while replacement-focused coverage prioritizes long-term reliability and upgrades. This side-by-side guide helps homeowners evaluate scope, costs, and timing so you can make an informed decision.

What is repair or replacement coverage?

Repair or replacement coverage refers to protection plans, warranties, or service contracts that help cover the cost of fixing or replacing household systems and appliances when they fail. In practical terms, you pay a premium or service fee to access coverage when a unit breaks down, and the policy outlines what is repaired, what is replaced, and under what conditions. For homeowners and renters, understanding how these coverages operate is crucial to avoiding gaps during a repair event. The Home Repair Guide team emphasizes that recognizing the difference between repair-focused and replacement-focused coverage can save time, money, and disruption. In many real-world scenarios, the decision hinges on the item’s expected life, the likelihood of future failures, and the balance between upfront costs and long-term value. The Home Repair Guide analysis shows that clarity on scope, exclusions, and claim processes often determines whether coverage meets your needs.

Why coverage decisions matter for homeowners

Coverage decisions matter because they shape how quickly you can access help, how much you pay out of pocket, and whether upgrades are included. A robust repair plan can quickly restore function after an ordinary failure without forcing a full system replacement. On the other hand, replacement coverage can protect against repeated repairs and the risk of sudden breakdowns, especially for aging components. The strategic choice should reflect your household’s tolerance for risk, your appliance age, and your budget cadence. Home Repair Guide’s experience with dozens of homeowner claims suggests that most households benefit from a balanced approach: cover the most failure-prone items with repair options, and reserve replacement coverage for items nearing end-of-life or with high replacement costs.

How coverage is structured

Most programs outline three core elements: covered items, exclusions, and the claim process. Coverage might apply to parts and labor for repairs, and in some cases it includes full or partial replacement if repair is not cost-effective. Deductibles or service call fees may apply, and certain items require documentation such as model numbers, purchase dates, and maintenance history. Home Repair Guide notes that the precision of these terms materially affects your out-of-pocket costs and claim success. A well-structured plan will also specify whether upgrades (e.g., energy-efficient models) are eligible upon replacement.

Repair vs replacement: key differentiators

- Scope of protection: Repair coverage usually targets specific failures with replacement as a fallback, while replacement coverage often broadens the protection to include major components or entire units.

- Economics: Repair often implies lower upfront costs but can accumulate over time; replacement may require higher premiums but reduces ongoing repair bills and downtime.

- Timing: Repairs are typically faster, but for older equipment the time to source compatible parts can delay service; replacement can take longer due to procurement but yields a newer unit with potential efficiency gains.

- Upgrades: Replacement coverage frequently allows newer models or improved efficiency, whereas repair coverage may keep you on the same unit longer.

- Eligibility: Some policies require documented maintenance history or age thresholds to trigger replacement, preventing early or unnecessary swaps.

These differentiators matter because they affect both immediate convenience and long-range value. The goal is to match your home’s operating profile with a plan that minimizes risk while maximizing predictable costs.

Cost considerations: upfront vs long-term value

Costs come in several forms: premiums or service fees, deductibles, and potential out-of-pocket costs not covered by the policy. A repair-focused plan typically has lower upfront premium and faster claims for minor issues, translating to less disruption. Replacement coverage often costs more upfront but reduces the chance of repeated repairs and can lock in upgrades or improved efficiency. Home Repair Guide analysis shows that evaluating lifetime value—how many repairs you avoid and how often you upgrade—helps determine which path offers the best balance. Consider the item’s age, historical failure rate, and expected maintenance costs when weighing options.

Common exclusions and gaps to watch

No policy covers every scenario. Common exclusions include wear from neglect, pre-existing conditions, cosmetic damage, and events outside normal use. Some plans exclude certain high-end or specialty appliances, or limit coverage to specific brands or models. Always check for caps on payouts, limits on replacement terms, and whether there are separate deductibles for repair versus replacement. The Home Repair Guide team recommends a careful read of exclusions and a candid discussion with the provider to map out worst-case scenarios and your expected lifespan of critical systems.

How to evaluate a policy: a step-by-step guide

- List your high-value and failure-prone items. 2) Compare coverage scope, exclusions, and claim procedures. 3) Assess the replacement eligibility criteria and upgrade options. 4) Consider maintenance history and future longevity. 5) Evaluate premium vs deductible trade-offs and auto-renew terms. 6) Check for bundled benefits like annual tune-ups or energy efficiency upgrades. 7) Read customer reviews and look for transparent claim outcomes. This stepwise approach helps translate policy language into practical consequences for your household.

Case scenarios: when repair makes sense and when replacement is better

Scenario A: A seven-year-old dishwasher develops intermittent leaks. If your coverage prioritizes repair and there’s no significant wear, a repair might be cost-effective. Scenario B: A fifteen-year-old HVAC system shows frequent failures and efficiency concerns. Replacement coverage could yield long-term savings and better energy performance, making a replacement a prudent choice. Scenario C: You’re renovating and want quieter, more efficient appliances. Replacement coverage may be attractive here, especially if upgrades are included. These scenarios illustrate how timing, age, and reliability shape the decision.

How to compare providers: practical checklist

- Confirm coverage scope for common failures and exclusions for each major component. - Verify claim turnaround times and any required documentation. - Ask about maintenance requirements to keep coverage active. - Seek clarity on deductibles, caps, and premium renewal terms. - Consider upgrade options and compatibility with existing systems. - Review customer service quality and the policy’s overall value over 5–10 years. A rigorous checklist helps you compare apples to apples.

Policy optimization: negotiating terms and maximizing value

When negotiating, request explicit language on what triggers replacement versus repair, and push for broader coverage on upgrades or energy-efficiency improvements. Ask for flexible upgrade options and a straightforward process for claims, including prompt on-site inspection and rapid procurement where possible. Maintain documentation of maintenance and receipts to support future claims. A proactive approach, aligned with your home’s lifecycle, can yield a policy that protects against unexpected costs while supporting sensible upgrades.

Real-world lessons from repairs and replacements

Across dozens of homeowner claims, the most valuable insights come from understanding policy language, the actual failure history of devices, and the communication quality of the provider. In practice, homeowners report that plans with clear replacement criteria and fast diagnostics reduce downtime and stress. Conversely, vague terms and limited coverage often lead to sticker shock when a claim is denied or only partially covered. The core lesson is to align protection with your home’s expected life cycles and maintenance discipline.

Practical steps to update coverage now

- Inventory your appliances and major systems, noting age and condition. - Gather maintenance records and purchase receipts to support claims. - Compare at least three providers, focusing on coverage scope, exclusions, and claim processes. - Request a written summary of replacement eligibility and upgrade options. - Decide on a target plan that balances premium, deductible, and expected repairs over the next 5–10 years.

Final tips for maximizing value and avoiding gaps

Keep maintenance up to date, document issues promptly, and review your coverage annually. If a policy allows, negotiate enhancements that cover upgrades and energy-efficient replacements. Sharing your home’s long-term plans with your provider can help tailor a coverage approach that minimizes risk and maximizes value. The goal is a sustainable balance between predictable costs and reliable performance.

Comparison

| Feature | Repair coverage | Replacement coverage |

|---|---|---|

| Cost dynamics | Lower upfront payments for service calls and parts | Higher upfront premiums with broader protection |

| Coverage scope | Typically covers repairs, parts, and labor for common failures | Covers replacement when repair is not feasible or cost-effective plus major components |

| Claim process | Faster turnaround for simple repairs and routine issues | Longer lead times due to sourcing parts or a replacement unit |

| Upgrade eligibility | Limited upgrades; often no bundled model changes | Often includes newer models or upgraded components upon replacement |

| Lifespan alignment | Can extend life of existing equipment with timely fixes | Aligns with longer-term reliability and efficiency improvements |

| Best for | Budget-conscious households seeking quick fixes | Homeowners prioritizing long-term durability and upgrades |

Upsides

- Lower upfront costs and faster service for common faults

- Preserves existing equipment and minimizes downtime

- Easier budgeting with predictable service terms

- Potential for flexible upgrade options in some plans

Disadvantages

- May incur higher long-term costs if failures accrue

- Limited coverage on major failures or upgrades without replacement terms

- Deductibles and service fees can add up over time

- Some policies require age or maintenance prerequisites to trigger replacement

Repair coverage is generally best for reducing immediate costs; replacement coverage shines for long-term reliability and upgrades.

Choose repair coverage to minimize short-term outlays and downtime. If your appliance or system is aging or you value upgrades and future-proofing, replacement coverage offers greater long-term protection and potential efficiency gains.

FAQ

What exactly is repair or replacement coverage?

Repair coverage pays for fixing specific failures, while replacement coverage covers replacing components or units when repair isn’t practical. Both aim to reduce out-of-pocket costs and downtime, but their triggers and limits vary by policy. Understanding the terms helps you align protection with your home’s lifecycle.

Repair coverage pays to fix failures; replacement coverage pays to replace a unit when repair isn’t practical. Read the policy to understand what triggers each path.

Does replacement coverage always mean a full replacement?

Not always. Some policies offer partial or staged replacements depending on the failure, cost, and feasibility. Always check what constitutes a replacement trigger and whether upgrades are included.

Replacement may be partial or staged; confirm the exact trigger and upgrade options with your provider.

Can I have both repair and replacement coverage?

Yes. Some providers offer bundled plans that include repair and replacement coverage for different item types. This can provide flexible protection, but verify the overall cost and what items are covered under each portion.

Bundles can mix repair and replacement coverage—just check what’s included and the costs.

How does coverage affect monthly premiums?

Generally, broader coverage or lower deductibles raise monthly premiums. If you’re cost-sensitive, weigh the premium against the expected repair and replacement costs you’d face without coverage.

Wider coverage usually means higher premiums; weigh this against expected repair costs.

What items are typically covered?

Plans usually cover major household systems (like HVAC, plumbing, electrical) and common appliances. Always review the excluded lists to avoid surprises during a claim.

Expect coverage for major systems and appliances; check exclusions carefully.

What should I do before filing a claim?

Document the issue with photos, note dates and maintenance performed, and contact the provider as soon as a failure is observed. Having this information speeds up the claim review.

Document the issue and maintenance history; contact the provider promptly.

Key Takeaways

- Assess item age and failure history before choosing coverage

- Compare coverage scope, exclusions, and claim terms carefully

- Estimate lifetime value, not just annual premium

- Ask about upgrade options with replacement coverage

- Keep maintenance records to support claims