How Much Is Credit Repair? Costs, Options, and Budgeting

Discover how much credit repair typically costs, from upfront fees to monthly charges and yearly estimates. Home Repair Guide analyzes 2026 pricing guidance to help homeowners budget and compare options.

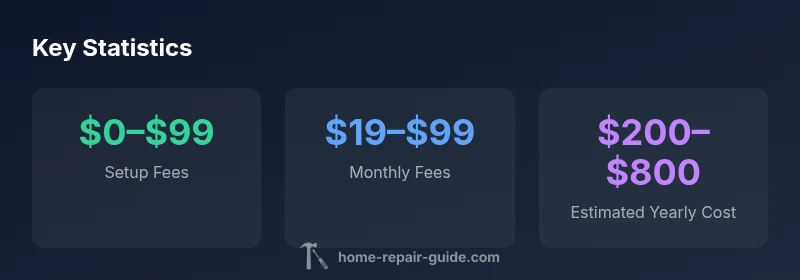

Typical upfront setup fees for credit repair range from $0 to $99, with ongoing monthly service fees usually between $19 and $99. When you total a year of service, expect roughly $200 to $800 in costs, varying by provider, dispute scope, and whether you DIY or hire professionals. This quick snapshot helps you plan before committing.

How much is credit repair: Cost basics

When homeowners and renters ask how much is credit repair, they want a simple answer, but the price depends on several factors. At its core, credit repair services help you dispute items on your credit report and negotiate with creditors. The cost picture often breaks into an upfront component and ongoing monthly charges, with a possible one-time add-ons for expedited results. According to Home Repair Guide, understanding the price structure starts with distinguishing between DIY steps and professional services. If you choose to do some work yourself, you can significantly reduce out-of-pocket costs, but you will invest more time. In 2026, most legitimate providers offer transparent pricing with ranges rather than fixed fees, which helps you budget for the year ahead. Understanding how much is credit repair really costs can help you decide between DIY and professional paths.

The Home Repair Guide team emphasizes that pricing varies by dispute scope and service level, so a one-size-fits-all quote is rare. Before committing, request a written breakdown that shows exactly what is included in the price, and whether the cost covers all filings, letters, and negotiations.

Cost components you should expect

Pricing for credit repair typically includes several components. First, upfront or setup fees can range from zero to about ninety-nine dollars, covering initial report review and service setup. Second, ongoing monthly fees usually cover dispute letters, creditor outreach, and monitoring; these fees commonly fall in the range of about twenty dollars to ninety-nine dollars per month. Third, some providers charge per item disputed or per item removed, which means your total cost grows with the number of items you challenge. Fourth, add-ons and expedited services can push costs higher if you want faster results or extra letters and verifications. In 2026, many providers publish transparent, range-based pricing rather than fixed fees, which helps buyers compare options. When evaluating offers, ask for a detailed bill of materials that shows exactly what is included and whether the price covers all filings, correspondence, and any guarantee of results.

DIY options and price impact

Doing credit repair yourself is possible and can dramatically reduce costs, but it requires time, organization, and a careful approach. You can begin by ordering your own credit reports and drafting dispute letters to address inaccurate accounts with the bureaus and creditors. Free templates exist, and some non-profit counseling services can help at low or no cost. The trade-off is patience: professional services may move disputes more swiftly and provide ongoing monitoring, but you’ll pay more for convenience. If you pursue DIY, plan for several hours per week for correspondence, tracking, and following up, and consider investing in basic record-keeping tools or affordable software to stay organized. Savings can be meaningful if you are disciplined and methodical, but the risk of errors remains a real consideration.

How credit repair interacts with home buying and financing

Good credit matters when applying for a mortgage. Credit repair can influence loan approvals and interest rates, potentially shaving thousands from lifetime costs if it yields a better rate. However, results depend on the lenders and the overall debt profile, and there’s no universal guarantee that every item will come off a report. If you’re planning to buy a home, coordinate your credit repair efforts with your mortgage broker early, so you understand timing and closing implications. In some cases, creditors require updated reports close to the loan application date, and you may need to schedule disputes accordingly. The interplay between credit repair, credit scoring, and loan terms is complex, but proactive planning can improve your odds of a favorable outcome.

How to compare providers and read contracts

To avoid surprises, compare providers using a simple checklist: pricing breakdown, service scope, dispute handling, and refund or cancellation policies. Look for clear language about what constitutes a completed dispute and what guarantees are offered. Read the contract for any automatic renewals, annual increases, or hidden fees, and verify whether you can pause or cancel services without penalties. Ask for a sample dispute letter pack and a timeline showing typical milestones. Finally, request references or case studies and verify claims with independent reviews when possible. A careful, written comparison makes it easier to select a plan that aligns with your budget and expectations.

Practical steps to reduce costs and maximize value

- Start with a free credit report review to identify obvious errors.

- Choose a provider that offers a clear price breakdown and no hidden fees.

- Consider a hybrid approach: handle straightforward disputes yourself while leaving complex cases to professionals.

- Set a monthly spending cap and track every charge to avoid drift.

- Build a longer-term plan that aligns with major milestones, such as a home purchase or refinancing. The Home Repair Guide team recommends comparing quotes, reading disclosures, and choosing a plan that fits your budget and goals.

Pricing models for credit repair services

| Model Type | Typical Cost Range | Notes |

|---|---|---|

| Flat fee | $0–$99 upfront | One-time setup and basic disputes |

| Monthly subscription | $19–$99 per month | Ongoing dispute work & monitoring |

| A la carte per item | $50–$150 per item | Per deletion or item removed |

FAQ

What is the typical upfront cost for credit repair?

Most providers charge $0–$99 upfront. Some offer free consultations or bundled services. Always verify what the upfront covers and whether the initial fee applies to ongoing work.

Yes, upfront fees are commonly zero to ninety-nine dollars; always check what’s included.

Are credit repair services regulated?

Credit repair services are governed by consumer protection laws; verify licensing, disclosures, and refunds. Avoid guarantees and ensure you understand your rights under the Fair Credit Reporting Act.

Yes, there are protections; check disclosures and refunds.

How long does credit repair take?

Results vary. Dispute activity can show changes in 3–6 months, but some items take longer or require creditor verification. Be cautious of timelines promised by providers.

Most improvements happen in a few months, but timelines aren’t guaranteed.

Can I do credit repair myself?

Yes, you can file disputes with credit bureaus and creditors yourself. It costs little beyond your time, but it requires perseverance and organization.

Yes, you can do it yourself, though it takes effort.

Do credit repair services guarantee results?

No legitimate service can guarantee removal of accurate negative items. Beware promises that sound too good to be true.

No guarantees on outcomes; be skeptical of guarantees.

How does credit repair affect home buying?

Improved credit can lead to better loan terms, lower interest rates, and easier approval. It is not a guaranteed fix for every lender.

Better credit often helps with rates, but isn’t a guarantee.

“Price is important, but the real value comes from disciplined dispute work and clear improvements on your credit reports.”

Key Takeaways

- Budget for upfront and ongoing costs to avoid surprises.

- Ask about scope to estimate total yearly costs.

- Compare DIY options vs paid services for best value.

- Read contracts and disclosures before signing.

- The Home Repair Guide team recommends getting written quotes.