Repair versus Capital Improvement: A Practical Guide

An objective, practical comparison of repairs versus capital improvements, outlining costs, value impact, and decision factors to help homeowners choose wisely.

Repair vs capital improvement isn't a one-size-fits-all decision. Repairs maintain function and prevent deterioration, often at a lower upfront cost, while capital improvements add long-term value and resilience but require higher upfront investment. The best choice depends on budget, property condition, and long-term goals. Consider whether you want immediate usability, potential tax incentives, and neighborhood expectations.

Defining repair vs capital improvement

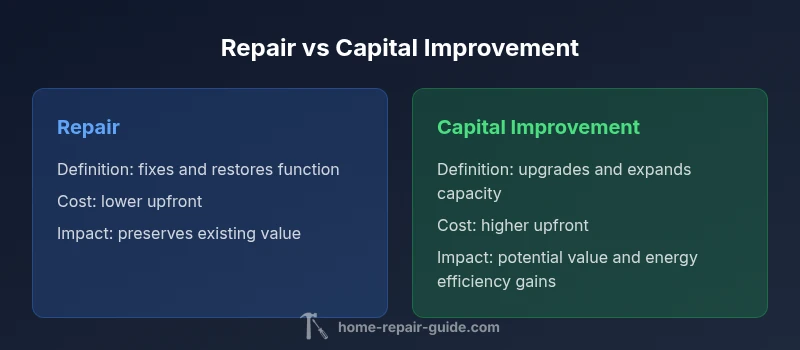

At its core, the distinction between repair and capital improvement determines how a homeowner budgets, plans, and values the work. According to Home Repair Guide, a repair is a targeted fix that restores a function or stops a deficit without changing the underlying structure or long-term value of the home. A capital improvement, by contrast, expands capacity, upgrades systems, or extends the asset’s life, thereby enhancing value and resilience. This difference matters not only for immediate costs, but also for long-term maintenance, insurance, and resale considerations. When you decide between repair versus capital improvement, you are weighing the balance between preserving what exists and investing in what will endure. In practice, most households confront both types of work over a property’s life: quick fixes that keep the house usable, and strategic upgrades that raise comfort, efficiency, and market appeal. Home Repair Guide’s approach is to help homeowners categorize projects early, estimate likely costs, and build a budget that reflects both short-term needs and long-term goals. Being clear about the distinction reduces confusion during planning and helps you communicate with contractors, lenders, and insurers. It also supports a more predictable maintenance schedule, which preserves the home’s value over time.

Financial implications: cost, value, and depreciation

From a budgeting perspective, repairs and capital improvements sit on different financial trajectories. Repairs typically demand smaller, more frequent outlays that restore function or prevent immediate risk. They are usually expensed through regular household cash flow and may not produce a direct increase in property value. Capital improvements, by contrast, involve larger upfront expenditures that enhance the home's capacity, efficiency, or aesthetics and can influence resale value. Because the initial outlay is higher and the work is more invasive, homeowners often plan these projects with a longer time horizon and financing strategies that spread costs over years. In many jurisdictions, tax treatment may differ between repairs and improvements, and some upgrades—such as energy efficiency investments—can qualify for credits or rebates. Home Repair Guide analysis shows that a structured budgeting approach, including a project log, cost estimates, and a staged implementation plan, helps homeowners avoid over-investment or underfunding. When evaluating options, consider not only the sticker price but also ongoing maintenance, potential energy savings, and the opportunity to align upgrades with current codes and future needs. A deliberate mix of repairs and improvements often yields the best balance between safety, usability, and value growth.

Impact on property value and insurance

Immediate repairs protect the property’s current condition, reducing the risk of further damage and potential insurance claims. However, most repairs do not automatically lift market value in the way that upgrades to windows, insulation, or a major bathroom remodel might. Capital improvements can raise appraisal values, improve energy efficiency, and enhance curb appeal—all factors that buyers consider. Insurance implications differ as well: some repairs prevent additional damage that could trigger higher premiums, while many capital improvements may qualify for endorsements or affect dwelling coverage differently when the policy is renewed. It’s important to document completed work and keep receipts, since lenders and insurers may request proof of scope and materials. The goal is to maintain a stable baseline that preserves capital while positioning the home for future growth. Home Repair Guide emphasizes that value is not guaranteed by any single project; rather, it emerges from a thoughtful program that combines necessary repairs with selective upgrades aligned to risk reduction and long-term market expectations.

Practical decision rules: when to repair vs when to invest in capital improvements

When choosing between repair versus capital improvement, many homeowners rely on a simple decision framework. Step 1: list the problem and its expected lifespan; Step 2: estimate immediate cost and long-term maintenance; Step 3: assess the potential impact on safety, comfort, and energy efficiency; Step 4: evaluate whether the project would be considered an addition or significant upgrade by appraisers and buyers; Step 5: check available financing options and any incentives. A rule of thumb is to treat any fix that restores function but does not materially improve performance as a repair, and any fix that changes structure, capacity, or efficiency as an improvement. For rental properties, consider depreciation and potential tax benefits. For owner-occupied homes, emphasize durability and energy savings. It can be helpful to prioritize improvements that address chronic inefficiencies or safety concerns first, then stage upgrades over time to spread out costs. Finally, communicate with your contractor using a clear scope of work and a written budget to avoid scope creep and surprise fees.

Examples across rooms and systems

- Kitchen: A leaky faucet is a repair; replacing old cabinets and upgrading to energy-efficient appliances is a capital improvement.

- Bathroom: Repairing a cracked tile or fixing a faulty toilet is a repair; installing a new vanity with improved plumbing and better ventilation is an improvement.

- Roofing: Patching a minor leak is a repair; replacing the roof or adding new underlayment is a capital improvement.

- Windows and insulation: Replacing single-pane windows or adding attic insulation is an improvement; resealing a window frame or caulking small gaps is a repair.

- Electrical and plumbing: Replacing a blown fuse or fixing a loose outlet is a repair; upgrading electrical panel capacity or updating piping to reduce corrosion is an improvement.

- Exterior doors and weatherproofing: Replacing a worn door with a new energy-rated model is an improvement; weather-stripping and caulking small gaps are repairs.

Planning and budgeting approach: a step-by-step method

- Define goals: Determine whether the aim is to reduce energy costs, improve comfort, or increase resale value. 2) Inventory and categorize: List every project and label as repair or improvement. 3) Gather estimates: Get written quotes from licensed professionals for scope clarity. 4) Prioritize: Rank by safety impact, return on investment, and alignment with long-term plans. 5) Create a phased plan: Schedule repairs first, then schedule capital improvements. 6) Build a contingency: Include a cushion for unexpected issues. 7) Track progress: Use a simple project log to compare actual costs vs estimates. 8) Review and adjust: Reassess budgets after each phase and adjust future plans accordingly.

Tax and incentives landscape: incentives, credits, and deductions

Although rules vary by jurisdiction and property type, some capital improvements may qualify for tax incentives, utility rebates, or energy-efficiency credits. Home Repair Guide recommends checking local programs and consulting a tax professional before assuming any deduction or credit. Even without credits, improvements such as better insulation or efficient heating and cooling systems can reduce energy bills and, over time, improve owner satisfaction and resale appeal. Record all receipts, permits, and code-compliant work to simplify future claims with insurers or lenders. In rental properties, depreciation rules may apply to improvements, which can help spread the cost over the asset’s life. Keep in mind that eligibility criteria and deadlines change, so stay current with official sources and guidance from reputable organizations, including government websites and university extension services.

Longevity, maintenance, and durability

Durable improvements reduce ongoing maintenance costs; however, all projects require routine care. Upgrading components with longer lifespans—such as mechanical systems, insulation, or roof ventilation—can lower long-term upkeep and energy use. Repairs, by contrast, often demand more frequent attention if the underlying condition is aging or if water intrusion and corrosion are not addressed. A maintenance schedule helps: inspect critical systems annually, schedule professional tests for safety-critical elements, and plan replacements before failure. Involving homeowners early in the planning phase fosters realistic expectations about performance and longevity. The key is to balance durability with cost and convenience, so you can enjoy reliable operation without overextending your budget.

How Home Repair Guide analyzes this topic

Home Repair Guide takes a practical, evidence-based view of repair versus capital improvement. We emphasize clear definitions, real-world examples, and budgeting tools you can adapt. Our guidance accounts for regional cost variations, homeowner goals, and the trade-offs between immediate safety and long-term value. We present both sides of the equation with equal weight, show how to quantify benefits like energy savings or durability, and provide checklists to help you plan, execute, and document projects. Our approach helps homeowners avoid common pitfalls such as scope creep, underfunded repairs, or over-improved spaces that don’t align with market expectations. While specific price figures will vary, the underlying principles—value, risk, and feasibility—remain consistent across properties and budgets.

Decision framework recap and quick checklist

Use a simple, repeatable process: categorize projects, estimate costs, assess impact, and plan a staged approach. Build a two-column budget; track repairs separately from improvements; check eligibility for incentives; and maintain good records. End with a clear timeline and a realistic contingency. A short checklist helps: define goal, categorize, obtain quotes, prioritize, schedule, document, reassess.

Authority sources

For further context, consult authoritative resources from government and education sources. The U.S. Department of Energy provides guidance on energy efficiency improvements and related incentives. The Internal Revenue Service explains how certain capital improvements may qualify for tax credits or deductions. University extension programs offer region-specific cost guidance and best practices for budgeting and project management. Example sources include:

- https://www.energy.gov

- https://www.irs.gov

- https://extension.university.edu

Comparison

| Feature | Repair | Capital Improvement |

|---|---|---|

| Definition | Focused fix restoring function without changing structure | Upgrades or expansions that add value or extend life |

| Typical scope | Restore current condition | Upgrade systems, capacity, or aesthetics |

| Initial cost range | Lower upfront cost | Higher upfront cost |

| Long-term cost impact | Lower ongoing maintenance in many cases | Potentially higher maintenance but longer life |

| Impact on property value | Maintains usability and safety | Can increase resale value and equity |

| Tax treatment / incentives | Repairs generally not tax-advantaged | Some improvements may qualify for credits/deductions in certain contexts |

| Disruption during work | Typically shorter, less invasive | May require more extensive disruption |

| Best For | Preserving function with minimal investment | Long-term value and efficiency gains |

Upsides

- Lower upfront costs for repairs

- Faster implementation and less planning

- Maintains safety and usability with minimal risk

- Less disruptive to daily life

- Clear path to addressing urgent issues

Disadvantages

- Limited impact on long-term value

- May accumulate ongoing maintenance costs

- Does not modernize or improve efficiency where needed

- Risk of under-investing in aging homes

Capital improvements generally deliver higher long-term value; repairs protect function and prevent damage.

When you want lasting equity and energy efficiency, prioritize improvements. If immediate usability and budget control matter more, start with repairs and plan upgrades as part of a staged strategy.

FAQ

What is the fundamental difference between a repair and a capital improvement?

A repair fixes a problem to restore function without changing the property's fundamental structure or value. A capital improvement adds value by upgrading systems, capacity, or aesthetics and often extends the asset's life. The distinction guides budgeting, financing, and potential value impact.

A repair fixes what’s broken; a capital improvement upgrades and adds value to your home.

Is a kitchen remodel a repair or a capital improvement?

A kitchen remodel is typically a capital improvement because it changes functionality, efficiency, and value. Smaller fixes like repairing a cabinet hinge are repairs. The scale and impact determine which category applies.

A kitchen remodel is generally an improvement; fixing a hinge is a repair.

Do repairs ever increase home value?

Repairs mainly preserve existing value and prevent further loss. In some cases, completing essential repairs improves perceived safety and condition, which can support value, but the effect is usually smaller than a well-planned improvement.

Repairs protect value; major improvements drive higher value.

How do repairs affect insurance coverage?

Repairs can reduce future claims by preventing damage, potentially stabilizing premiums. Capital improvements may alter policy terms or endorsements, especially if they affect risk profiles like insulation or roof upgrades. Always update your insurer after major work.

Repairs reduce risk; upgrades may change coverage terms.

What factors should guide the decision between repair and capital improvement?

Key factors include safety impact, cost and financing options, expected lifespan, energy efficiency, and how the project aligns with long-term plans. A formal cost-benefit approach helps avoid over- or under-investing.

Consider safety, cost, lifespan, and long-term goals when deciding.

Are there tax incentives for capital improvements?

Some jurisdictions offer tax credits or rebates for energy-efficient improvements. Eligibility varies by location and property type, so check official programs and consult a tax professional before proceeding.

Some incentives exist; check local programs and consult a tax pro.

Key Takeaways

- Classify projects as repairs or improvements before budgeting

- Use a two-track budget: immediate fixes plus future upgrades

- Prioritize upgrades with energy savings and durability

- Document work for insurance and resale

- Reference authoritative sources for incentives and guidance